PMI and MIP represent private home loan insurance and home mortgage insurance premium, respectively. Both of these are kinds of home mortgage insurance to safeguard the lending institution and/or investor of a mortgage. If you make a deposit of less than 20%, mortgage financiers impose a mortgage insurance coverage requirement. In many cases, it can increase your monthly payment of your loan, however the flipside is that you can pay less on your deposit.

FHA loans have MIP, that includes both an in advance home mortgage insurance premium (can be paid at closing or rolled into timeshare pros and cons the loan) and a month-to-month premium that lasts for the life of the loan if you only make the minimum down payment at closing. Getting prequalified is the first step in the home mortgage approval procedure.

But, because income and possessions aren't confirmed, it just functions as a price quote. Seller concessions involve a clause in your purchase arrangement in which the seller consents to help with certain closing costs. Sellers could accept pay for things like real estate tax, lawyer charges, the origination charge, title insurance coverage and appraisal.

Payments are made on these bills when they come due. It used to be that banks would hold on to loans for the whole term of the marriott timeshare rentals loan, however that's progressively less common today, and now most of home loan are offered to one of the significant home mortgage financiers think Fannie Mae, Freddie Mac, FHA, and so on.

Quicken Loans services most loans. A home title is evidence of ownership that likewise has a physical description of the home and land you're buying. The title will also have any liens that provide others a right to the property in particular scenarios. The chain of title will reveal the ownership history of a particular home.

Mortgage underwriting is a phase of the origination process where the lending institution works to confirm your income and possession info, financial obligation, along with any property details to release last approval of the loan. It's essentially a process to assess the quantity of threat that is related to giving you a loan.

website >What Does What Is The Debt To Income Ratio For Conventional Mortgages Do?

With validated approval, your deal will have equal strength to that of a money purchaser. The procedure begins with the same credit pull as other approval phases, however you'll likewise have to supply documentation including W-2s or other earnings verification and bank declarations.

Forbearance is when your home loan servicer or loan provider permits you to stop briefly (suspend) or lower your home mortgage payments for a restricted amount of time while you restore your financial footing - which of the following statements is true regarding home mortgages?. The CARES Act supplies numerous homeowners with the right to have all home mortgage payments totally paused for a duration of time.

You are still required to repay any missed out on or lowered payments in the future, which in the majority of cases might be paid back with time. At the end of the forbearance, your servicer will call you about how the missed out on payments will be paid back. There might be different programs available. Ensure you comprehend how the forbearance will be repaid.

For instance, if you have a Fannie Mae, Freddie Mac, FHA, VA, or USDA loan, you won't have to repay the amount that was suspended all at onceunless you are able to do so (what is today's interest rate for mortgages). If your income is brought back before completion of your forbearance, connect to your servicer and resume paying as quickly as you can so your future commitment is restricted.

Eager to benefit from traditionally low rate of interest and purchase a home? Getting a home loan can constitute your biggest and most meaningful monetary deal, but there are several steps associated with the process. Your credit history informs lenders just just how much you can be depended repay your mortgage on time and the lower your credit report, the more you'll pay in interest." Having a strong credit report and credit report is necessary since it suggests you can receive beneficial rates and terms when using for a loan," states Rod Griffin, senior director of Public Education and Advocacy for Experian, one of the 3 major credit reporting agencies.

Bring any past-due accounts current, if possible. Evaluation your credit reports for free at AnnualCreditReport. com as well as your credit history (often available totally free from your charge card or bank) a minimum of three to 6 months before making an application for a mortgage. When you receive your credit rating, you'll get a list of the leading elements impacting your rating, which can inform you what modifications to make to get your credit in shape.

The 15-Second Trick For Why Do Banks Sell Mortgages To Other Banks

Contact the reporting bureau instantly if you find any. It's enjoyable to think about a dream home with all the trimmings, however you should try to only buy what you can reasonably manage." Most experts think you need to not invest more than 30 percent of your gross regular monthly income on home-related expenses," says Katsiaryna Bardos, associate professor of financing at Fairfield University in Fairfield, Connecticut.

This is identified by summing up all of your month-to-month debt payments and dividing that by your gross monthly income." Fannie Mae and Freddie Mac loans accept a maximum DTI ratio of 45 percent (what are the different types of mortgages). If your ratio is higher than that, you might wish to wait to purchase a home up until you lower your financial obligation," Bardos recommends.

You can determine what you can pay for by using Bankrate's calculator, which consider your earnings, monthly commitments, estimated deposit, the information of your mortgage like the rates of interest, and house owners insurance coverage and property taxes. To be able to manage your regular monthly real estate costs, which will consist of payments towards the mortgage principal, interest, insurance and taxes along with maintenance, you ought to prepare to salt away a large amount.

One basic guideline of thumb is to have the equivalent of approximately 6 months of mortgage payments in a cost savings account, even after you fork over the deposit. Don't forget that closing expenses, which are the charges you'll pay to close the home mortgage, typically run in between 2 percent to 5 percent of the loan principal.

In general, goal to save as much as possible until you reach your preferred deposit and reserve savings goals." Start little if necessary but remain committed. Attempt to prioritize your cost savings prior to investing on any discretionary products," Bardos recommends. "Open a different represent down payment savings that you don't use for any other expenditures.

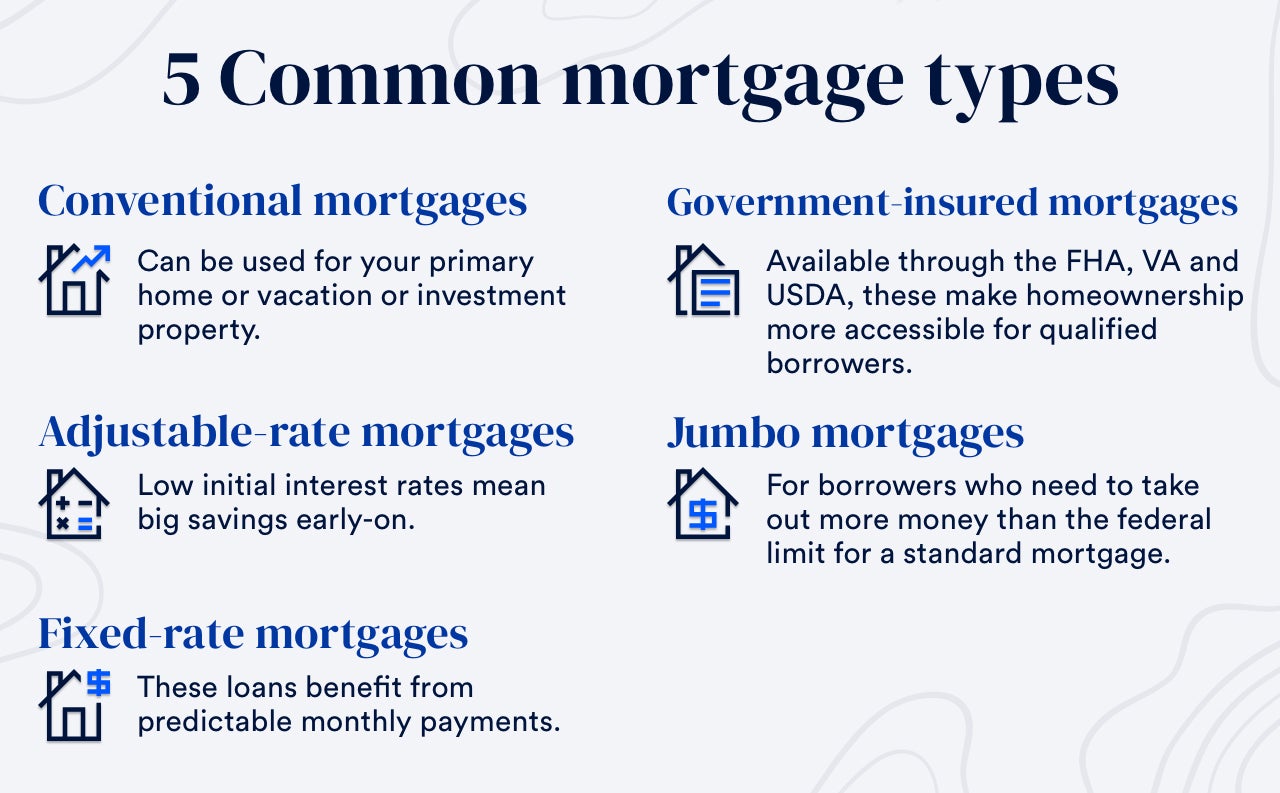

The primary kinds of mortgages include: Traditional loans Government-insured loans (FHA, USDA or VA) Jumbo loans These can be either fixed- or adjustable-rate, suggesting the interest rate is either repaired for the period of the loan term or changes at fixed periods. They commonly come in 15- or 30-year terms, although there might be 10-year, 20-year, 25-year or even 40-year home loans available.

What Is The Current Libor Rate For Mortgages Things To Know Before You Get This

5 percent down. To find the best lender, "speak with pals, relative and your representative and ask for recommendations," recommends Guy Silas, branch supervisor for the Rockville, Maryland workplace of Embrace Home Loans. "Likewise, search rating sites, perform internet research study and invest the time to genuinely check out consumer evaluations on lenders." [Your] decision ought to be based on more than just price and rates of interest," nevertheless, states Silas.